Since 2005, the market for Health Savings Accounts (HSAs) and qualified high deductible health plans has been continuously growing, and so has the market for HSA management services.

However, TPAs who want to compete and make money by adding HSAs to their portfolio see significant barriers to market entry — finding revenue opportunities, time and cost involved, and multiple business partnerships, among others. To avoid these pitfalls to success, TPAs need a solution that can help them streamline HSA administration and deliver a better experience to their clients and account holders.

Introduction

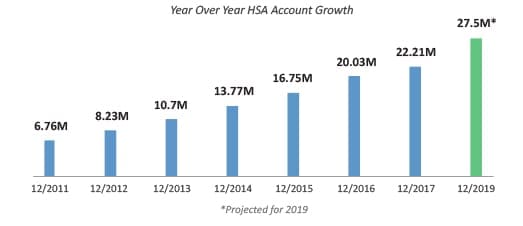

Since 2005, the Health Savings Account (HSA) market has seen continuous year-over-year growth. Tied directly to the increase in high deductible health plan (HDHP) enrollment, the number of HSA accounts has grown from 6.76 million in 2011 to 22.21 million in 20171, a 228 percent increase during that period. The market is projected to reach 27.5 million accounts by the end of 2019.

Despite a steadily growing market and positive forecasts, many TPAs remain cautious about offering HSA management services. Among their concerns are startup costs, competing with banks and rival HSA providers, and providing superior customer service without sacrificing other business needs. Perhaps their biggest concerns, however, involve potential barriers to market entry. The three largest perceived obstacles include:

- Finding revenue opportunities within the market

- Funding the incremental administrative work involved

- Identifying and working with a custodial banker

To address these concerns, many HSA technology providers have sought to overcome these challenges with various solutions that offer an array of banking and investing partnerships. Unfortunately for TPAs, managing separate relationships with HSA technology providers, custodial banks, and investment firms creates a patchwork of partnerships that must be maintained over time, increasing costs and support headaches. To simplify HSA administration, keep costs low, and maximize profits, TPAs need a turnkey solution with streamlined, comprehensive account management functionality.

Is there money to be made in HSA administration?

The chief causes of apprehension with administering HSAs are the time, workload, and costs involved. HSA management expenses can include software, personnel, enrollment meetings, expense certification, and more. Despite these concerns, however, HSA administration costs are relatively low compared to other tax-advantaged CDH accounts.

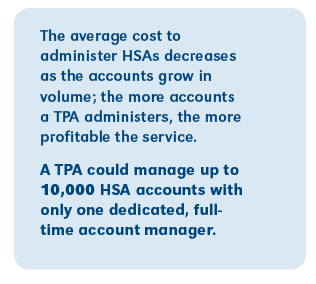

In a recent study completed by DataPath, it was determined that HSA administration costs about $1.75 per account (on average) for small to mid-size TPAs. That includes the software platform, personnel, support costs, card services, and other general operating expenses. Furthermore, the average cost to administer HSAs decreases as the accounts grow in volume; the more accounts a TPA administers, the more profitable the service.

In comparison to FSAs, HSA administration is more scalable. Administrators can dedicate fewer resources – personnel, hardware, etc. — to HSAs than it takes for FSA or HRA administration. DataPath’s study discovered that it takes approximately 20 hours per week to manage 5,000 accounts. A TPA could manage between 5,000 – 10,000 HSAs with only one dedicated account manager (40 hours per week), adding one full-time account manager per every 10,000 accounts.

Another important factor in determining whether or not there is money to be made in HSA administration involves how much revenue can be generated by managing these accounts. There is a common misconception that many providers, particularly banks, do not charge a monthly fee for HSAs. However, the myth of the ‘free’ HSA is not entirely true.

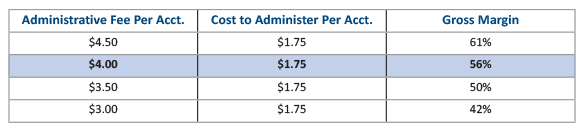

According to Devenir2, seven out of ten of the largest HSA providers in the nation charge an account maintenance fee, ranging from $2.00-$4.50. Some of these providers reduce their maintenance fees as the account balance grows, though more than half continue to charge fees even when balances exceed $2,000. According to the Employee Benefit Research Institute3, over 50 percent of all HSA account holders have balances under $1,000 and more than two-thirds have balances under $2,000. So, even with a balance of $2,000, six out of ten of these providers continue to charge an administrative fee.

Since most of the market is accustomed to paying administrative fees for HSAs, TPAs can justifiably charge a reasonable fee and generate significant revenue and profitability. For example, if a TPA charged a $4.00 administrative fee per account, with actual costs being $1.75 per account, the TPA could see a gross margin of 56 percent. The following chart provides a profitability comparison based on several revenue scenarios.

Multiple Banking and Investing Options

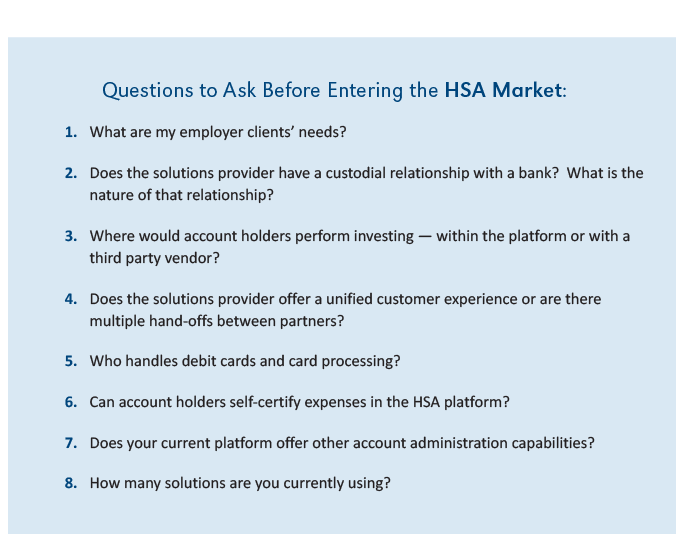

In attempting to address the challenges TPAs face in starting up HSA management services, many technology providers tout administration solutions that support multiple banking and investment partner options. On the surface, the flexibility sounds appealing; however, having multiple partner relationships with technology providers, banks, and investment firms creates a patchwork HSA account management system. This HSA management “frankensystem” can create a variety of unforeseen problems, as the piecemeal relationships can lead to confusion, ambiguity, and frustration for employers and account holders.

Compound costs and uncertainty – TPAs need to charge for account administration. If they outsource banking and investment services, those partners also have their own business needs and profitability goals. Fees can vary from one partner to the next, leaving the employer to pay multiple charges or passing on account fees to their employees. For the employer or employee, the increased expense and uncertainty can result in aggravation and dissatisfaction.

Unclear investment advice – HSA owners need confidence to invest. With so many available options, which partner does the account holder trust most? Can the employer be sure that its employees are getting the best service and advice? If a bank doesn’t provide investment options, then the TPA has to find another partner, or leave it up to employers or account holders to fend for themselves.

Card providers – Some platform providers issue the cards themselves, while others allow the bank to do it. Question is, who performs card processing? Since most solutions providers are not end-to-end card processors, they must outsource many of the other card-related processes. This is another handoff in the chain of relationships, further complicating transparency and simplicity.

Muddled accountability – When there are multiple relationships involved in a single process, it greatly complicates where accountability lies. If there’s an issue, who does the TPA or the account holder call to get a resolution?

Weakened security – Card and account security is a major concern for individuals. With information being passed from one source to another, there is greater risk of security breakdowns. As with accountability, who is responsible when sensitive information is compromised?

Customer “service” – TPAs need stellar customer service to help their companies thrive. To address this need, some technology solution providers offer outsourced call centers or a “white label” customer relationship service for their clients. However, can these outside entities best represent the TPA? This type of service just adds another entity to the patchwork of partnerships that account holders must navigate for problem resolution, not to mention having to utilize numerous web portals to manage a single account.

With so many intertwined relationships, there is inherent uncertainty for end users – TPAs, employers, and HSA participants. Who manages whom in order to deliver a cohesive experience? In contrast, partnering with a solutions provider that offers all HSA services and management functions in a single platform can overcome these potential pitfalls and deliver greater peace-of-mind and user satisfaction across the board.

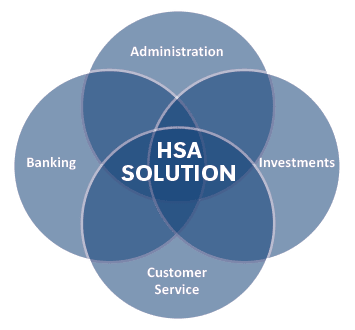

Single Platform for HSA Management, Banking, Card Services, and Investments

Finding a solutions partner that centralizes the entire HSA process through established relationships can provide a bevy of improvements for TPAs, employers, and account holders over the multi-partnership approach.

Known costs – A single provider with a custodial banking relationship can provide more stability when it comes to cost. There are no surprises, and they can negotiate the fees up front, allowing TPAs and employers to have a better handle on cost expectations.

Lower fees – In addition to known fees, having fewer relationships should translate into lower costs for employers because it reduces overhead and eliminates redundant expenses.

Centralized portal – HSA administration, banking, and investments in a single portal ensures that your clients get the “all-in-one” experience. They don’t have to visit multiple vendor websites to manage one account. A unified, cohesive experience generates higher overall satisfaction.

In-house investments – A single solutions provider, which includes investment services, should have licensed investment and financial personnel to oversee financial operations, including reviewing and establishing investment portfolios, and providing educational materials for participants. Employers and account holders can have the confidence that their needs are being addressed up front, and it’s one less relationship for them to manage.

Greater accountability – A ‘one-stop shop’ for every HSA need gives everyone greater accountability into the process – including HSA management, banking, investments, and customer service. There is only one point of contact, making problem resolution faster, easier, and more transparent.

Improved security – An end-to-end card and payment processor handles every part of the process in-house. By reducing the transfer of information, there are much tighter security controls involved and less risk of data being compromised. This translates into greater peace of mind for both employers and employees.

Superior customer service – Providing excellent customer service is key to any successful business. Being straightforward about who is providing customer support not only builds goodwill amongst everyone involved, but also provides a quality experience. There is no guessing game as to who is on the other end and there’s a single point of contact.

Conclusion

For HSA management solutions, TPAs have many choices. One option is to piece together an administration system by selecting multiple partners for technology platforms, custodial banking, investments, and other outsourced services. This method provides a sense of flexibility, but can also lead to greater problems when it comes to cost, user experience, customer service, accountability and more. With choice after choice, what guarantees can a TPA provide to employers and account holders?

HSA administration does not have to be complicated, and neither does the “solution.” Another option is to choose an all-in-one solutions provider with HSA management, custodial banking, and investments, all packaged together into a single platform. Optimally, for any TPA who also offers other benefits administration such as FSAs, HRAs, Transit, COBRA, etc., a true all-in-one platform is the icing on the cake. The “one-stop shop” for HSA management provides a seamless and more satisfactory experience for each party involved.

TPAs have the confidence that they’re delivering superior service and a solid platform to their employer clients, with fewer headaches. Employers can rest easy, knowing that their workforce is receiving a terrific benefit with excellent customer service. HSA participants have a single point of contact for all their HSA-related needs, from banking, card services, investments, and administration.

About the Company: For 40 years, DataPath has been a pivotal force in the employee benefits, financial services, and insurance industries. The company’s flagship DataPath Summit platform offers an integrated solution for managing CDH, HSA, Well-Being, COBRA, and Billing. Through its partnership with Accelergent Growth Solutions, DataPath also offers expert BPO services, automation, outsourced customer service, and award-winning marketing services.

1 2017 Year-End HSA Market Statistics & Trends Executive Summary, Devenir Research

2 Devenir, https://www.hsasearch.com/hsa-providers/hsa-provider-lists

3 Health Savings Account Balances, Contributions, Distributions, and Other Vital Statistics, 2016: Statistics from the EBRI HSA Database